Making Tax Digital (MTD): Complete UK Guide for 2026

Making Tax Digital is the biggest change to how the UK reports tax in a generation. If you are a sole trader, a landlord, or you run a small business, you have probably seen the letters “MTD” in an HMRC email and wondered what it actually means for you.

This guide walks through what Making Tax Digital is, who it applies to, when your deadlines land, and what you need to do to get ready. We will keep things simple and practical, with no jargon left unexplained.

Quick answer: Making Tax Digital is HMRC’s programme to move tax reporting online. It requires digital record keeping and, depending on the tax, either quarterly or regular digital submissions through approved software. VAT has used MTD since 2022. Income Tax Self Assessment joins the programme from 6 April 2026 for people with qualifying income above £50,000.

What Is Making Tax Digital?

What does Making Tax Digital mean?

Making Tax Digital, often shortened to MTD, is HMRC’s plan to move tax record keeping away from paper and spreadsheets and onto approved digital software. Instead of gathering a year of receipts and filing one big tax return, people inside MTD keep digital records throughout the year and send updates to HMRC at set points.

The rules do not apply to every tax at once. VAT has been part of MTD since 2019, and it became compulsory for all VAT-registered businesses in 2022. Income Tax is joining next, in phases, starting from 6 April 2026. Corporation Tax was considered for MTD too, but HMRC confirmed in 2025 it will not go ahead with a mandatory scheme.

Why HMRC introduced Making Tax Digital

HMRC’s reasoning is straightforward: paper records and one-off annual returns leave more room for mistakes. A study by the National Audit Office found that errors and lack of care in tax returns cost the UK billions of pounds in lost revenue each year. By asking people to keep digital records as they go and report more often, HMRC hopes to catch errors earlier, reduce the scale of the “tax gap,” and give taxpayers a clearer view of what they owe throughout the year rather than a shock in January.

There is also a practical side for taxpayers. Quarterly updates mean you build a running picture of your income and expenses instead of reconstructing a full year from memory in January. Many accountants say this makes budgeting for a tax bill considerably easier once you get into the rhythm of it.

How Making Tax Digital works

At its core, MTD rests on three requirements that apply across the different taxes it covers:

- Digital record keeping. You keep records of income and expenses in software rather than on paper or in a basic spreadsheet, unless that spreadsheet is linked to bridging software that can send data straight to HMRC.

- Digital submissions. Instead of typing figures into HMRC’s website by hand, your software sends the data directly, using what is called an Application Programming Interface, or API, link.

- More frequent reporting. VAT returns are typically still quarterly. Income Tax under MTD moves from one annual return to four quarterly updates plus a year-end Final Declaration.

The exact mechanics differ by tax, which is why the sections below cover VAT, Income Tax, and Corporation Tax separately.

Who Needs to Use Making Tax Digital?

Not everyone is affected in the same way or at the same time. Here is a breakdown by group.

Sole traders

If you are a sole trader, MTD applies to you through MTD for Income Tax once your qualifying income passes the relevant threshold for your tax year. Qualifying income means your total turnover from self-employment and property combined, before you deduct any expenses or allowances. It is not your profit.

Self-employed individuals

The term “self-employed” covers sole traders as well as anyone else running a trade or profession on their own account, such as freelancers, consultants, and tradespeople. The same qualifying income thresholds and quarterly reporting rules apply.

Landlords

Landlords with UK or overseas property income are included in MTD for Income Tax on the same basis as the self-employed. If your rental income and any self-employment income together exceed the threshold for your tax year, you will need to comply. This applies whether you own one rental property or several, though all UK property income is combined into a single reporting stream.

Partnerships

General partnerships are not yet mandated into MTD for Income Tax. HMRC has confirmed that partnerships will be brought in at a later date, though no start date has been set. Individual partners with their own separate self-employment or property income outside the partnership may still need to comply for that income.

Limited companies

Limited companies pay Corporation Tax, not Income Tax, on their profits. HMRC shelved its plans for MTD for Corporation Tax in 2025 and confirmed there is no mandatory start date. Companies continue to file the CT600 as they do now. That said, a director who also has personal rental income or a side sole trade may still fall within MTD for Income Tax for that personal income, separate from the company’s own filing.

Individuals

Individuals who only receive employment income through PAYE, pension income, dividends, interest, or capital gains are not affected by MTD for Income Tax. Those income types do not count towards the qualifying income threshold. MTD is aimed specifically at self-employment and property income.

Making Tax Digital for Income Tax

What is MTD for Income Tax?

Making Tax Digital for Income Tax, sometimes written as MTD for ITSA (Income Tax Self Assessment), replaces the single annual Self Assessment return with digital record keeping, four quarterly updates, and a Final Declaration at the end of the tax year. It applies to people with income from self-employment, property, or both.

The rollout began on 6 April 2026 after more than a decade of delays and design changes. Around 860,000 taxpayers were expected to be affected in the first year, with that figure projected to grow to roughly three million as the income threshold falls over the coming years.

Who qualifies?

Whether you need to join depends on your qualifying income in a specific earlier tax year, not the current one. HMRC checks the tax return you submitted before your phase begins:

| Qualifying income threshold | Tax year assessed | You must comply from |

|---|---|---|

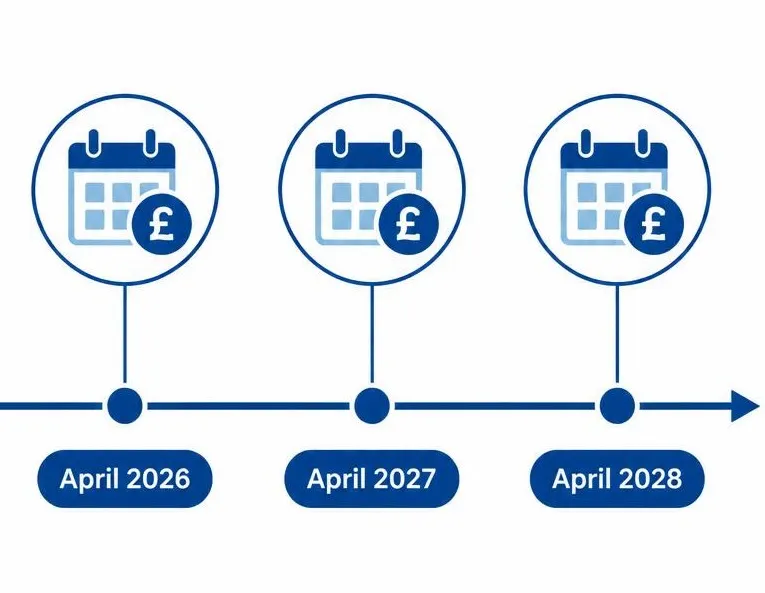

| Over £50,000 | 2024 to 2025 | 6 April 2026 |

| Over £30,000 | 2025 to 2026 | 6 April 2027 |

| Over £20,000 | 2026 to 2027 | 6 April 2028 |

If your income later drops below the threshold, you generally stay within MTD once you have been brought in, though there is an exemption route if your reported receipts fall to £20,000 or less for three years running.

What is qualifying income?

Qualifying income is your gross turnover from self-employment and UK property combined, before you take off any expenses, allowances, or reliefs. If you have both a trade and a rental property, HMRC adds the two together to test against the threshold. For example, someone with £29,000 in trading receipts and £22,000 in gross rental income has £51,000 in qualifying income, which places them above the first threshold even though neither source alone would.

Income that does not count towards this test includes employment income taxed under PAYE, pension income, dividends, interest, and capital gains.

Quarterly updates explained

Once you are in MTD for Income Tax, you send a quarterly update to HMRC for each business or property source you have. This is a running summary of income and expenses for that three-month period, not a full tax calculation. If you have both a self-employment and a property source, each one needs its own update.

By default, HMRC uses standard tax year quarters, and the deadlines are the 7th of the month following the end of each quarter:

- 6 April to 5 July, due 7 August

- 6 July to 5 October, due 7 November

- 6 October to 5 January, due 7 February

- 6 January to 5 April, due 7 May

Some software allows you to choose calendar quarters instead, which can make life easier if your bookkeeping already runs on calendar months.

End of Period Statement (EOPS)

Design changes announced in Autumn 2023 removed the separate End of Period Statement for most taxpayers, folding that step into the Final Declaration instead. In practice, this means most people under MTD for Income Tax now finalise their figures, claim reliefs, and confirm their year end position in one step rather than two, which simplifies the process compared with earlier proposals.

Final Declaration

After your four quarterly updates for the tax year, you submit a Final Declaration. This is the MTD equivalent of the old Self Assessment return. It is where you confirm your full year figures, correct any provisional numbers from your quarterly updates, claim allowances and reliefs, and add any non-qualifying income such as dividends or employment earnings. The deadline is 31 January following the end of the tax year, the same date that has always applied to Self Assessment. For the 2026 to 2027 tax year, the first Final Declaration under MTD is due by 31 January 2028.

Tax payment dates themselves have not changed. You still pay by 31 January and, where payments on account apply, by 31 July.

Making Tax Digital for Landlords

Which landlords must comply?

Any landlord, whether they let one property or a portfolio, is treated the same way as a sole trader for MTD purposes. What matters is your combined qualifying income from property and any self-employment, tested against the threshold for your phase.

Income thresholds

The same three-stage threshold applies to landlords as to the self-employed: £50,000 from April 2026, £30,000 from April 2027, and £20,000 from April 2028. A landlord earning £57,000 in gross rental income in the 2024 to 2025 tax year, for instance, falls into the first phase and must comply from April 2026.

Digital record keeping

Landlords need to record rental income and allowable expenses digitally using MTD-compatible software, or a spreadsheet paired with bridging software that can transmit the data to HMRC. Paper ledgers and basic spreadsheets on their own are no longer sufficient once you are within the scope of MTD.

One useful easement for jointly owned property: if you own a property with someone else, you can exclude the related expenses from your in-year quarterly updates and account for them at the Final Declaration stage instead, which cuts down on some of the admin around shared costs.

Reporting requirements

All UK property income, even across multiple properties, is combined into one property reporting stream. You do not need to file a separate quarterly update for each individual property, only for each type of business, so a landlord with three rental properties still only submits one property update per quarter, alongside a separate update if they also run a sole trade.

Making Tax Digital for VAT

Who must register?

MTD for VAT is already fully in force and has applied to every VAT registered business, regardless of turnover, since April 2022. If you are VAT registered, you are required to follow MTD rules, with only a small number of exemptions available, mainly for businesses where digital record keeping is not reasonably practical due to age, disability, location, or religious belief.

VAT record keeping

Businesses must keep certain records digitally, including the time of supply, the value of supply, and the rate of VAT charged for each transaction. These records need to sit in software, or in a spreadsheet that links to HMRC through bridging software.

VAT submissions

VAT returns continue to be filed at the same frequency as before, most commonly quarterly, though some businesses file monthly or annually under special schemes. The change under MTD is not how often you file, but how: your MTD-compatible software sends the return data directly to HMRC through a digital link, rather than you retyping figures into HMRC’s online portal by hand.

Digital links

HMRC requires an unbroken digital link from the point a transaction is first recorded through to the final VAT return figure. This means that if your data moves between different pieces of software or spreadsheet tabs, that transfer needs to happen digitally, for example through a formula or an export and import process, rather than someone manually retyping numbers at any stage. Manually retyping figures partway through the chain breaks the digital link and can put you outside the rules.

Making Tax Digital for Corporation Tax

Is Corporation Tax included?

No, not at present. HMRC consulted on extending MTD to Corporation Tax back in 2021, exploring the idea of digital record keeping and quarterly updates similar to the Income Tax model. Following that consultation, HMRC decided not to proceed. This was confirmed formally in HMRC’s 2025 Transformation Roadmap, which stated that MTD for Corporation Tax will not be introduced.

Future plans

Rather than a mandatory MTD scheme, HMRC says it intends to modernise Corporation Tax administration more broadly, including updated internal systems and improved digital services, without imposing quarterly reporting on companies. Limited companies continue to file their CT600 annually, with tax due nine months and one day after the end of the accounting period, exactly as before. If you run a limited company but also have personal rental or self-employment income outside it, remember that your personal income could still bring you into MTD for Income Tax, separate from how your company reports Corporation Tax.

Making Tax Digital Deadlines

Current MTD deadlines

The clearest way to think about MTD deadlines is to separate them by tax, since VAT, Income Tax, and the (shelved) Corporation Tax plans each have their own timeline.

Income Tax rollout

- 6 April 2026: MTD for Income Tax becomes mandatory for anyone with qualifying income over £50,000 in the 2024 to 2025 tax year.

- 6 April 2027: The threshold drops to £30,000, based on the 2025 to 2026 tax year.

- 6 April 2028: The threshold drops again to £20,000, based on the 2026 to 2027 tax year.

VAT deadlines

VAT has no further threshold changes on the horizon. It has applied to all VAT registered businesses since April 2022, and the existing filing frequency (usually quarterly) continues as normal under the digital rules.

2026 implementation

For anyone newly mandated from 6 April 2026, the first quarterly update covers 6 April to 5 July 2026 and is due by 7 August 2026. HMRC has confirmed a “soft landing” for the 2026 to 2027 tax year: no penalty points will be issued for late quarterly updates during this first year, though you must still submit them, since all four are needed before you can file your Final Declaration. The soft landing does not cover the Final Declaration itself or late payment penalties, so those still follow the normal rules.

Late submission penalties work on a points system. Each missed deadline adds one point, and reaching four points triggers a £200 fine. Points expire after a period of compliant filing. Late payment penalties are separate and are based on a percentage of the tax owed: broadly 3% of the outstanding amount at 15 days overdue, a further 3% at 30 days, and 10% a year on anything still outstanding after that.

How to Register for Making Tax Digital

HMRC registration process

You do not need to wait for a letter from HMRC to register, though HMRC has been writing to people it believes meet the £50,000 threshold based on their most recent tax return. Not receiving a letter does not mean you are exempt. It remains your responsibility to check whether your income puts you within scope.

Sign up steps

To register for MTD for Income Tax, you will generally need to:

- Confirm your qualifying income for the relevant tax year to check which phase applies to you.

- Choose HMRC-recognised software, either a full accounting package or bridging software linked to a spreadsheet.

- Sign up through HMRC’s online service, or have your accountant do this on your behalf as your agent.

- Authorise the connection between your chosen software and HMRC.

For MTD for VAT, if you are newly VAT registering, you are generally set up for MTD automatically as part of registration, since it now applies to everyone in the VAT system.

Before you register

It is worth testing your chosen software before your mandatory start date. HMRC allows voluntary sign-up if you are below the threshold, which gives you the chance to get familiar with quarterly reporting without your bank account being permanently linked to HMRC. Many accountants recommend at least one full quarter of practice before your real obligations begin, so you catch any data or categorisation issues while the stakes are still low.

Making Tax Digital Requirements

Across VAT and Income Tax, the practical requirements come down to a short list:

- Digital records. Transactions need to be recorded in software, not on paper, and not in a plain spreadsheet unless it is linked to bridging software.

- Compatible software. HMRC maintains a list of recognised software providers. Popular options include Xero, QuickBooks, FreeAgent, and Sage, alongside specialist bridging tools for people who prefer spreadsheets.

- Quarterly submissions. VAT returns and Income Tax updates are sent directly from your software to HMRC through a digital link, on the schedule that applies to your tax.

- Record retention. Digital records generally need to be kept for at least five years for Income Tax purposes, in case HMRC asks to review them.

Frequently Asked Questions

When does Making Tax Digital start?

MTD for VAT has applied to all VAT registered businesses since April 2022. MTD for Income Tax starts on 6 April 2026 for people with qualifying income over £50,000, with further groups joining in April 2027 and April 2028 as the threshold falls.

Is Making Tax Digital mandatory?

Yes, for anyone who is VAT registered, and for anyone whose qualifying income from self-employment or property exceeds the relevant threshold for their phase. A small number of exemptions exist, mainly for people who are digitally excluded or hold specific types of income such as trust or non-resident income.

Do landlords need Making Tax Digital?

Yes, if their combined rental and self-employment income exceeds the threshold for their phase. A landlord earning above £50,000 in gross rental income in the 2024 to 2025 tax year must comply from April 2026, for example.

Does MTD apply to limited companies?

Not for Corporation Tax. HMRC shelved its plans for MTD for Corporation Tax in 2025, and companies continue to file the CT600 as before. A company’s VAT obligations are unaffected by this and MTD for VAT still applies if the company is VAT registered. Directors with personal property or self-employment income may separately fall within MTD for Income Tax.

Can I use spreadsheets?

Yes, but only if the spreadsheet is linked to HMRC-recognised bridging software that can transmit your data digitally. A spreadsheet on its own, with figures typed into HMRC’s portal by hand, does not meet the digital link requirement.

What happens if I don’t comply?

Missed submissions build up penalty points under a points-based system, with a £200 fine once you reach four points. Late payment of tax carries separate, percentage-based penalties that increase the longer the amount stays unpaid. For the first year of MTD for Income Tax (2026 to 2027), HMRC has said it will not issue penalty points for late quarterly updates, though the updates themselves are still required and the Final Declaration deadline is not covered by this easement.

A Final Word on Getting Ready

Do not leave this until the week before your first deadline. Check your qualifying income now against your most recent tax return, choose software early, and run a practice quarter if you can. Getting comfortable while the pressure is low makes the real deadlines far less stressful.

If your situation involves joint property ownership, mixed income sources, or a limited company alongside personal income, speak to an accountant who can confirm exactly which parts of MTD apply to you and when.

For related guidance on running a UK business, see our guides on Best Making Tax Digital Software in the UK, how to register a business in the UK and how to value a business.

About the author

Emma Radcliffe is a UK-based finance writer with seven years of experience covering small business tax and accounting topics, including HMRC compliance and digital record keeping for sole traders and landlords.