How to Write a Business Plan in the UK: A Step-by-Step Guide

If you are starting a business in the UK, a business plan is one of the first things you need to get right. It is not just paperwork. It is the document that shapes how you think about your idea, and it is often the difference between getting funding and getting rejected.

This guide walks you through exactly how to write a business plan in the UK, from the first page to the final numbers. You will find a clear structure, a simple example, and practical tips that lenders and investors actually look for.

What Is a Business Plan and Why Does It Matter

A business plan is a written document that sets out what your business does, who it serves, and how it plans to make money. It usually covers your objectives, your market, your marketing approach, and your financial forecasts.

You do not need a business plan only when you are chasing investment. It also gives you a working reference point. Many business owners return to their plan every few months to check progress and adjust their approach as the market changes.

There is a practical reason to take this seriously too. Lenders assessing government-backed Start Up Loans look closely at your business plan and financial forecasts rather than your trading history, since new businesses usually do not have one yet. A weak plan is one of the most common reasons applications get turned down.

If you have not yet registered your business, it is worth reading our guide on how to register a business with Companies House before you finalise your plan, since your legal structure affects several sections of it.

Who Actually Reads Your Business Plan

Before you write a single word, think about your audience. A bank manager wants proof you can repay a loan. An investor wants to see growth potential and a route to a return. A business partner wants clarity on roles and expectations.

You do not need a separate plan for each reader, but you can adjust the emphasis. If you are applying for a loan, spend more time on cash flow and repayment ability. If you are pitching to investors, spend more time on market size and growth strategy.

Quick answer: most UK business plans need to satisfy three readers at once: the writer (you), a lender or investor, and your future self checking progress a year from now.

Business Plan Formats: Which One Should You Choose

Not every business needs the same type of plan. Choosing the right format saves you time and keeps the document useful rather than something you write once and never open again.

Traditional Business Plan

This is the full, detailed format most banks and investors expect. It runs to 15 to 30 pages and covers every section in depth, including financial projections for three to five years. Use this format if you are applying for a Start Up Loan, approaching a bank, or seeking outside investment.

Lean Business Plan

A lean plan condenses your strategy into a few pages, often using a one-page canvas covering your value proposition, customer segments, costs, and revenue streams. It works well for testing an idea quickly or for internal planning when you do not need to convince a lender.

One-Page Business Plan

This is a single sheet summarising your business idea, target market, and key goals. It suits early-stage thinking or a quick pitch document, but it will not satisfy a bank or investor who needs full financial detail.

If you are unsure which format to choose, start with a lean plan to clarify your thinking, then expand it into a traditional plan once you are ready to apply for funding or a loan.

Business Plan vs Business Model

| Business Plan | Business Model |

|---|---|

| Detailed document | Framework explaining how the business makes money |

| Used for funding | Used for strategy |

| Includes financial forecasts | Focuses on value creation |

| Updated periodically | Can evolve frequently |

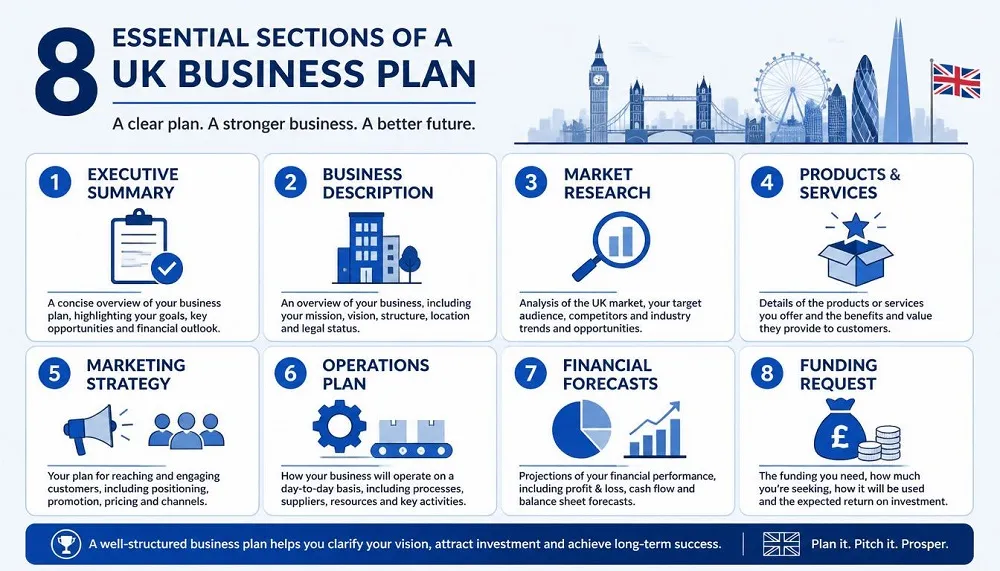

What Should a Business Plan Include

Most UK business plans, whatever the format, cover the same core ground. Here is what to include:

- Executive summary

- Business description and objectives

- Legal structure (sole trader, limited company, or partnership)

- Products or services

- Market research and competitor analysis

- Marketing and sales strategy

- Management team and structure

- Operations plan

- Financial projections and cash flow forecast

- Funding request (if applicable)

Every plan looks slightly different depending on the business, but missing any of these sections will weaken your document in the eyes of a lender.

| Section | Purpose |

|---|---|

| Executive Summary | Overview of the business |

| Business Description | Explain what the business does |

| Market Research | Demonstrate customer demand |

| Products & Services | Describe your offering |

| Marketing Plan | Explain how you’ll attract customers |

| Operations Plan | Outline daily business activities |

| Financial Forecast | Show expected income and costs |

| Funding Request | Explain how much funding you need |

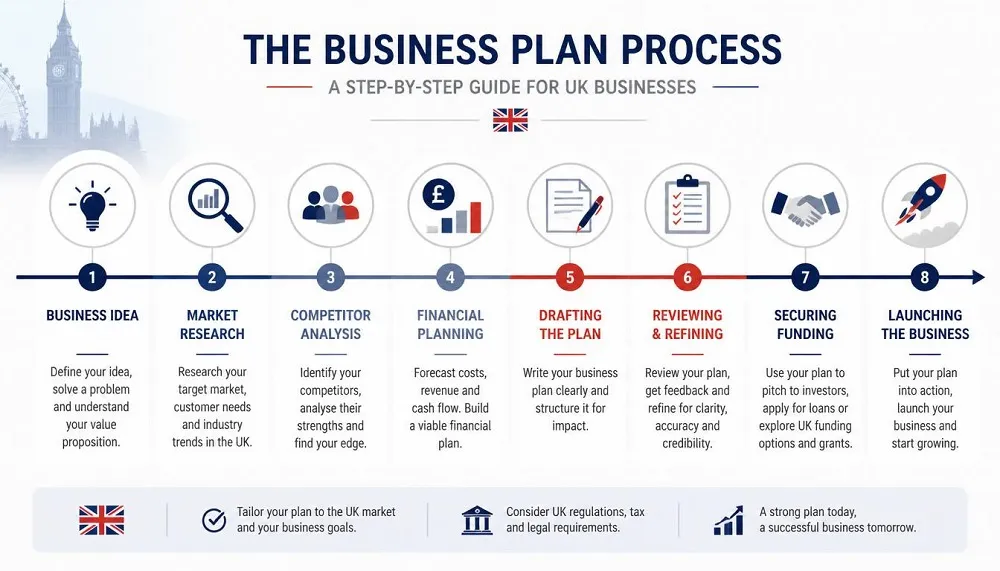

How to Write a Business Plan Step by Step

Here is the order that works best in practice. Writing sections in this sequence means you are not guessing numbers before you have done the research to support them.

Step 1: Write Your Executive Summary Last

The executive summary sits at the top of the document, but it should be the last thing you write. It is a short overview of your entire plan, usually no more than a page, covering your business idea, your objectives, and what makes your business worth backing.

Since this is often the only section a busy lender reads in full, keep it sharp. State what your business does, who it serves, and why it will succeed, in plain language.

Step 2: Describe Your Business and Legal Structure

Explain what your business is, what it sells, and where it operates. Include your legal structure here too. Whether you register as a sole trader or a limited company changes your tax position, your personal liability, and how lenders view your application.

If you have not decided yet, our guide on sole trader vs limited company in the UK breaks down the practical differences so you can choose the right structure before you finalise this section.

Step 3: Research Your Market

This section proves you understand who you are selling to and why they will buy from you rather than a competitor. Include your target customer profile, the size of your market, and a short competitor analysis.

Back up your claims with real figures where you can find them. Vague statements like “there is strong demand” carry little weight. A specific figure, even an estimate drawn from a trade report or government data, shows you have done the work.

Step 4: Explain Your Products or Services

Describe what you are selling in practical terms. What problem does it solve? What makes it different from what is already on the market? Keep this section focused on customer benefit rather than technical detail.

Step 5: Outline Your Marketing and Sales Strategy

Explain how customers will find out about your business and how you will convert interest into sales. Cover your pricing approach, your main marketing channels, and your plan for retaining customers once you have them.

You do not need a full marketing plan here. A clear, believable outline is enough. Save the detail for a separate marketing document if you need one.

Step 6: Introduce Your Management Team

Lenders and investors back people as much as ideas. List the key people involved, their relevant experience, and any gaps you still need to fill. Being upfront about a gap, such as needing to hire a bookkeeper in month four, shows foresight rather than weakness.

Step 7: Build Your Financial Projections

This is usually the section that decides whether your plan succeeds or fails with a lender. Include a sales forecast, a cash flow forecast, and a profit and loss projection covering at least the first year, ideally three.

Keep your assumptions realistic. Overly optimistic forecasts are one of the fastest ways to lose credibility with an experienced lender. If you are still working out your setup costs, our guide on startup costs for a small business can help you build accurate figures before you commit them to your plan.

Step 8: Add Your Funding Request

If you are seeking finance, state clearly how much you need, what it will be used for, and how you plan to repay it. Government-backed Start Up Loans currently offer between £500 and £25,000 per founder at a fixed interest rate, with up to £100,000 available across a founding team, and lenders assess these applications mainly on the strength of your plan and forecasts rather than your trading history.

A Simple Business Plan Example for a UK Startup

To make this concrete, here is a short example for a fictional mobile dog grooming business based in Leeds.

Executive summary: PawMobile offers on-demand dog grooming at customers’ homes across Leeds, targeting busy pet owners who want a convenient alternative to salon visits.

Market research: Leeds has an estimated 45,000 dog-owning households. Competitor research shows only two mobile grooming services currently operating in the area, both fully booked most weeks.

Financial projection: Year one target of 500 bookings at an average of £45 per booking, generating approximately £22,500 in revenue, with start-up costs of £8,000 covering a converted van and equipment.

Funding request: A £8,000 Start Up Loan to cover the van conversion and initial equipment, repaid over three years from booking revenue.

This is a simplified version, but it shows the structure: a clear idea, evidence behind it, and numbers that add up.

Writing a Business Plan for a Limited Company

If you are setting up as a limited company, your business plan needs a few extra details. Include your company registration number once you have it, your registered office address, and the shareholding structure if there is more than one director.

Lenders will also want to see how the company’s finances are kept separate from your personal finances, since this is a legal requirement for limited companies. If you have not yet set up your accounts, check our guide on business bank account requirements in the UK so this section of your plan reflects accurate, current information.

Using Your Business Plan to Get Funding

A business plan is central to almost every UK funding route. Bank loans, government-backed Start Up Loans, angel investment, and even some grants all expect to see one before they will talk numbers.

Lending data from 2025 and 2026 shows that fewer than half of UK loan applications from small businesses are currently approved, with approval rates well below pre-pandemic levels. Preparation makes a measurable difference here. A clear plan with realistic forecasts and evidence of demand puts you well ahead of applicants who turn up with a vague idea and no numbers.

If you are applying for a Start Up Loan specifically, note that the fixed interest rate on new applications increased from 6% to 7.5% in April 2026, and eligibility now covers businesses trading for up to 60 months rather than 36. Check the current terms before you finalise your funding request section, since rates and criteria do shift from year to year.

Free Business Plan Resources

Recommend resources such as:

- Government guidance

- Business support organisations

- Financial forecasting templates

- Accounting software

Common Business Plan Mistakes to Avoid

- Overly optimistic forecasts. Lenders have seen thousands of plans and can spot unrealistic numbers quickly.

- Ignoring competitors. Claiming you have no competition usually signals you have not researched the market properly.

- Writing for yourself, not the reader. Avoid industry jargon that only makes sense to you.

- Skipping the cash flow forecast. Profit looks good on paper, but cash flow is what keeps a business running day to day.

- Treating the plan as a one-off task. A plan left untouched for two years quickly becomes useless. Update it as your business changes.

How Long Should a UK Business Plan Be

There is no fixed rule, but most traditional UK business plans run between 10 and 20 pages. A lean plan can be as short as one or two pages. The right length depends on your purpose. A plan for a bank loan needs enough financial detail to satisfy an underwriter. A plan for your own use only needs enough detail to keep you on track.

Focus on what your reader needs rather than hitting a page count. A concise, well-evidenced ten-page plan will always beat a padded thirty-page document.

Frequently Asked Questions

Do I need a business plan if I am not seeking funding?

Yes, though it can be shorter. A business plan helps you clarify your goals, spot problems early, and measure progress even if you never approach a lender.

How often should I update my business plan?

Review it at least once a year, and update it sooner if something significant changes, such as a new competitor entering your market or a shift in your costs.

Can I write a business plan myself, or do I need an accountant?

You can write the plan yourself, but it is worth having an accountant check your financial projections before you submit it to a lender. Numbers that do not add up will undermine an otherwise strong plan.

What is the difference between a business plan and a business proposal?

A business plan is an internal and external strategy document covering your whole business. A business proposal is usually a shorter document aimed at winning a specific client, contract, or piece of funding.

Final Thoughts

Writing a business plan in the UK does not need to be complicated, but it does need to be honest and well researched. Work through each section in order, back up your claims with real figures, and save your executive summary for last. Whether you are applying for a Start Up Loan, approaching a bank, or simply mapping out your first year, a clear plan gives you a far stronger starting point than a good idea alone.

Before You Finish Your Business Plan

- Review your financial forecasts.

- Check all figures are consistent.

- Remove unnecessary jargon.

- Proofread for spelling and grammar.

- Ask someone else to review it.

- Update it regularly as your business evolves.

About the author

Sarah Mitchell is a UK-based business writer with 8 years of experience covering small business finance and startup planning. She has worked with early-stage founders across the UK on funding applications and financial forecasting.