Corporation Tax for Small Businesses in the UK: The Complete Guide

If you run a limited company in the UK, Corporation Tax is one bill you cannot avoid. It catches a lot of new directors off guard, mostly because nobody tells you the rules in plain English until you already owe money. This guide walks through exactly what Corporation Tax is, how much you will pay, when it is due, and how to stay on the right side of HMRC without paying more than you need to.

What Is Corporation Tax?

Corporation Tax is the tax that UK limited companies pay on their profits. It works in a similar way to how Income Tax applies to an individual’s wages, except here it is your company, not you personally, that owes the money. Every penny your business earns after expenses, whether from trading, investments, or selling an asset for more than it cost, falls within scope.

Unlike Income Tax, there is no tax-free personal allowance for companies. If your business makes a profit of £1, that £1 is technically taxable. In practice, allowable expenses and reliefs bring the real figure down considerably, which is why understanding what you can deduct matters just as much as understanding the rate itself.

Who Actually Has to Pay It

Corporation Tax applies to:

- UK limited companies, whether trading or not

- Foreign companies with a UK branch or office

- Clubs, societies, and associations that make a taxable profit

- Unincorporated associations in some circumstances

If your company is dormant, meaning it has stopped trading and has no income, you still need to tell HMRC. You will not owe tax, but silence is not an option; HMRC expects a formal notification either way.

Corporation Tax vs Income Tax for Sole Traders

This is where a lot of confusion starts. Sole traders and partnerships do not pay Corporation Tax at all. Instead, profits are taxed through Income Tax and National Insurance via Self Assessment. The moment you incorporate and start trading as a limited company, your business profits shift into the Corporation Tax system, and any money you then take out as salary or dividends becomes a separate personal tax matter on top of that.

This distinction is often the deciding factor when business owners weigh up whether to stay a sole trader or set up a limited company, since the tax treatment, filing obligations, and paperwork are genuinely different. If you are still deciding which structure suits you, our sole trader vs limited company guide breaks down the tax and legal differences in more detail.

Current Corporation Tax Rates in the UK

Since April 2023, the UK has run a two-tier Corporation Tax system rather than one flat rate for every company. Where your profits sit within that structure determines what you pay.

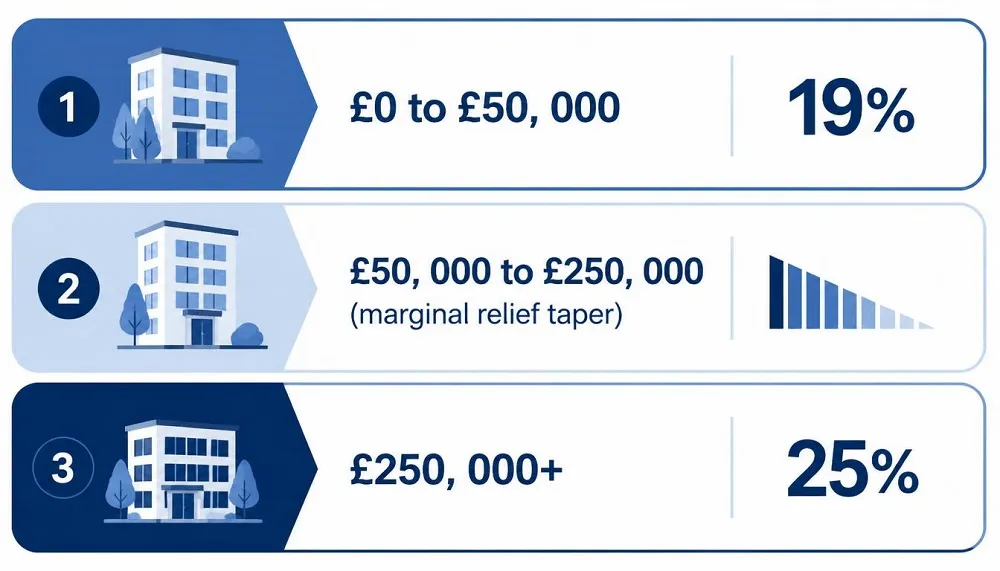

The Small Profits Rate

If your company’s taxable profits are £50,000 or less, you pay the small profits rate of 19%. This rate exists specifically to keep the tax burden lighter for genuinely small companies, and it has stayed at 19% since the two-tier system began.

The Main Rate

If your taxable profits exceed £250,000, you pay the main rate of 25%. This rate applies regardless of company size once profits cross that upper threshold, and it remains at 25% for the financial year beginning 1 April 2026.

Marginal Relief Explained in Plain English

Profits sitting between £50,000 and £250,000 do not simply jump from 19% to 25%. Instead, Marginal Relief tapers the rate gradually across that band, so your effective rate rises smoothly rather than in one big step. HMRC provides an online Marginal Relief calculator, but it helps to understand the logic behind the number it gives you.

Worked Example: Calculating Marginal Relief

Say your company made a taxable profit of £120,000 in the year. Because that falls between £50,000 and £250,000, you qualify for Marginal Relief. The calculation applies a fraction (currently 3/200) to the difference between the upper limit and your actual profit, then subtracts that from what you would owe at the main rate.

In practical terms, a £120,000 profit works out to an effective Corporation Tax rate somewhere between 19% and 25%, rather than a flat 25%. Compare that to a company making £40,000 profit, which sits below the £50,000 threshold and pays a straightforward 19%, or £75,600. A company making £300,000, above the upper threshold, pays the full 25% rate on the entire profit, coming to £75,000. The relief exists precisely to stop that jump feeling like a cliff edge for growing businesses.

If your company has associated companies, meaning other companies under common control, both the £50,000 and £250,000 thresholds are divided between them. Two associated companies effectively halve each threshold, so it is worth checking this carefully if your business structure includes more than one entity.

How to Work Out Your Taxable Profits

Your Corporation Tax bill is not based on your bank balance or your turnover. It is based on taxable profit, which takes some working out.

What Counts as Profit for Corporation Tax

Start with your total income for the accounting period: sales, service fees, interest earned, and any other money coming into the business. From that, deduct your allowable running costs such as rent, wages, software subscriptions, and marketing. What remains is your profit before tax.

Adjustments You Need to Make

Your accounting profit and your taxable profit are rarely identical. Certain costs that appear in your accounts, such as client entertainment, are not allowable for tax purposes and must be added back. Capital expenditure on equipment or vehicles is treated separately through capital allowances rather than as a straightforward expense. Chargeable gains from selling business assets also need to be folded into the calculation. This adjusted figure, not your raw accounting profit, is what your Corporation Tax rate actually applies to.

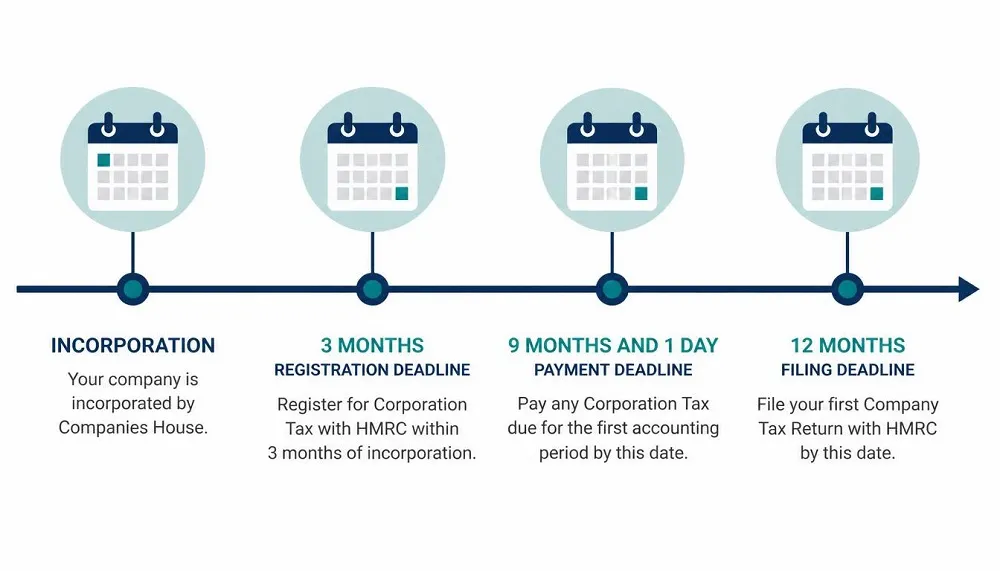

Registering for Corporation Tax

Once your company starts trading, receiving income, or otherwise becomes active, you must register for Corporation Tax with HMRC within three months. This applies even if you do not expect to owe any tax in your first year.

What Information HMRC Needs

When you register, you will need to provide:

- The date your company started trading (this becomes the start of your first accounting period)

- Your company name and registration number from Companies House

- Your registered office address

- The nature of your business activity

- Your main business address, if different from your registered office

Most companies are automatically set up for Corporation Tax shortly after incorporation, and HMRC issues a Unique Taxpayer Reference (UTR) that you will need for every future return. It is still worth checking your HMRC business tax account rather than assuming registration happened correctly. For a full walkthrough of the incorporation step itself, see our guide to registering a business with Companies House.

What Happens If You Register Late

Missing the three-month registration window can result in penalties calculated against any tax that ends up unpaid. It rarely causes serious trouble if caught early, but leaving it unaddressed compounds the problem, since HMRC will not know to expect a return from you and any resulting confusion tends to land back on the director.

Allowable Expenses and Reliefs That Reduce Your Bill

Nobody enjoys handing over a quarter of their profit to HMRC, so it pays to know exactly what you are entitled to claim before you calculate anything.

Common Deductible Expenses

To qualify, a cost must be “wholly and exclusively” for business purposes. Typical examples include staff salaries and employer National Insurance contributions, office rent and utilities, professional fees such as accountancy costs, travel directly related to business activity, and marketing spend. Employer pension contributions are also treated as a business expense and are exempt from Corporation Tax, which makes them a genuinely useful planning tool alongside the National Insurance savings they bring.

Capital Allowances

Money spent on equipment, machinery, or company vehicles is not deducted as a simple running cost. Instead, capital allowances let you offset this spending against your taxable profit, often at a generous rate for the year the purchase was made. If your business buys tools, computers, or a work vehicle, this is where the real savings usually sit.

Other Reliefs Worth Knowing About

Depending on your sector and activity, you may also be able to claim Research and Development relief, creative industry reliefs, or loss relief if your company made a loss in a previous period. These are worth discussing with an accountant, since eligibility rules are specific and claiming incorrectly can trigger a compliance check.

Filing Your Company Tax Return (CT600)

Once you know your taxable profit, that figure needs to be formally reported to HMRC through a Company Tax Return, known as the CT600.

What Goes Into a Company Tax Return

Your CT600 must include your company name and registration number, registered office address, tax reference number, turnover and profit for the period, your full tax calculation, and details of any allowances and reliefs claimed. Because taxable profit rarely matches your accounting profit exactly, most returns include a separate Corporation Tax computation showing how you adjusted from one figure to the other.

Filing With Companies House at the Same Time

Alongside your CT600 to HMRC, you must file annual accounts with Companies House. These are two separate obligations with two separate recipients, even though the deadlines often fall close together. From April 2026, the joint online filing service that let some companies submit to both organisations in one place is closing, so returns need to be prepared using commercial software or filed separately with each body.

Corporation Tax Deadlines You Need to Know

This is where most of the confusion, and most of the penalties, happen. There are two distinct deadlines, and mixing them up is a genuinely common mistake.

Payment Deadline

Corporation Tax itself is due nine months and one day after the end of your accounting period. For example, if your accounting period ends on 31 December, payment is due by 1 October the following year. Companies with profits above £1.5 million follow a different quarterly instalment system.

Filing Deadline

Your Company Tax Return (CT600) is due later, twelve months after the end of your accounting period. Using the same example, a period ending 31 December means your return is due by the following 31 December, a full three months after you were required to pay.

Why These Two Dates Are Different

It catches people out because it feels backwards: you have to pay before you have formally filed the return confirming how much you owe. In practice, this means you need to calculate your tax liability well ahead of the return deadline, since HMRC expects payment based on your own estimate, not on a figure they have already confirmed.

| Obligation | Deadline |

|---|---|

| Register for Corporation Tax | Within 3 months of starting to trade |

| Pay Corporation Tax | 9 months and 1 day after your accounting period ends |

| File Company Tax Return (CT600) | 12 months after your accounting period ends |

| File annual accounts with Companies House | 9 months after your financial year ends (21 months after incorporation for your first accounts) |

Penalties and Interest for Late Payment or Filing

HMRC does not send a warning before applying penalties, so it is worth building deadlines into your calendar well in advance rather than relying on memory.

Late Filing Penalties

Miss the CT600 deadline and a fixed penalty applies automatically, even if you owe no tax at all. From returns due on or after 1 April 2026, the initial penalty rises to £200, increasing to £400 if you are more than three months late, with steeper fixed penalties for companies that file late across three consecutive periods. Companies House applies its own separate penalty for late annual accounts, starting at £150 and doubling if you are late two years running.

Late Payment Interest

Missing the payment deadline does not trigger a fixed fine in the same way, but HMRC charges daily interest on the outstanding amount. On smaller bills this feels manageable, but interest compounds quickly on larger liabilities, so it is worth prioritising payment even if your return itself is not quite ready.

Corporation Tax If Your Company Makes a Loss

Making a loss does not remove your filing obligation. You must still declare it to HMRC through your Company Tax Return, even though there is nothing to pay. The upside is that trading losses can usually be carried forward and offset against profits in future years, which can meaningfully reduce your tax bill once the business turns a profit again. Some losses can also be carried back against the previous year’s profit in certain circumstances, so it is worth checking whether this applies to your situation before assuming the loss is simply gone.

Associated Companies and How They Affect Your Thresholds

If your company has one or more associated companies, meaning companies under shared control, the £50,000 and £250,000 profit thresholds are divided between them. Two associated companies halve each threshold to £25,000 and £125,000; three associated companies divide it further still. This catches out group structures and business owners running more than one active company, since it can push a business into the main rate or Marginal Relief band sooner than a single standalone company would experience.

Common Corporation Tax Mistakes Small Business Owners Make

A few mistakes come up again and again among first-time directors:

- Assuming Corporation Tax and the Company Tax Return share one deadline, when payment is due three months earlier than filing

- Forgetting to register within three months of starting to trade

- Confusing accounting profit with taxable profit and under or overpaying as a result

- Missing capital allowances on equipment or vehicle purchases

- Not accounting for associated companies when calculating which rate applies

- Leaving the Corporation Tax calculation until the return is almost due, rather than estimating early enough to pay on time

Most of these come down to timing rather than complexity. Building a simple calendar with your registration, payment, and filing dates removes the guesswork entirely. It is also worth tracking this alongside your other tax obligations, such as VAT registration, since growing businesses often need to manage both at once.

Should You Handle Corporation Tax Yourself or Hire an Accountant?

Plenty of small business owners manage straightforward Corporation Tax calculations themselves, particularly in the early years when the business is simple, and profits are modest. Where it usually makes sense to bring in an accountant is when you are claiming capital allowances, dealing with associated companies, carrying losses forward, or simply want confidence that your CT600 is accurate before it reaches HMRC. Even if you handle your own bookkeeping day to day, a professional review before filing can catch errors that are far cheaper to fix before submission than after.

Frequently Asked Questions

Do sole traders pay Corporation Tax? No. Sole traders and partnerships pay Income Tax and National Insurance through Self Assessment instead. Corporation Tax only applies once a business incorporates as a limited company.

How much Corporation Tax will my small business pay? It depends on your taxable profit. Profits up to £50,000 are taxed at 19%, profits above £250,000 at 25%, and anything in between is taxed at a tapered rate through Marginal Relief.

What happens if I miss the Corporation Tax payment deadline? HMRC charges daily interest on the unpaid amount from the day after the deadline until it is paid in full.

Can I reduce my Corporation Tax bill legally? Yes, through allowable expenses, capital allowances, pension contributions, and reliefs such as loss relief or Research and Development relief where your business qualifies.

Do I need to file a Company Tax Return if my company made a loss? Yes. A loss still needs to be declared to HMRC, even though no tax is due for that period.

Sarah Whitfield is a UK-based business finance writer with three years of experience covering small business tax, accounting, and compliance topics for owner-managed companies.