Start Up Loans UK: The Complete 2026 Guide to Rates, Eligibility and How to Apply

Starting a business usually comes down to one blunt question: where does the money come from. If you’ve searched for start-up loans UK, you’ve probably found a mix of government pages, comparison sites and lenders all telling you slightly different things. Some of it is out of date. The rate changed this year, and a few details that used to be true no longer are.

This guide sets out exactly how the UK’s Start Up Loans scheme works right now, what it costs, who can get one, and how it compares with grants and other finance. No filler, just what you need before you apply.

What Is a Start Up Loan in the UK?

A Start Up Loan is a government-backed personal loan for people starting or growing a business in the UK. It’s delivered through the Start Up Loans Company, a subsidiary of the British Business Bank, which is wholly owned by the government.

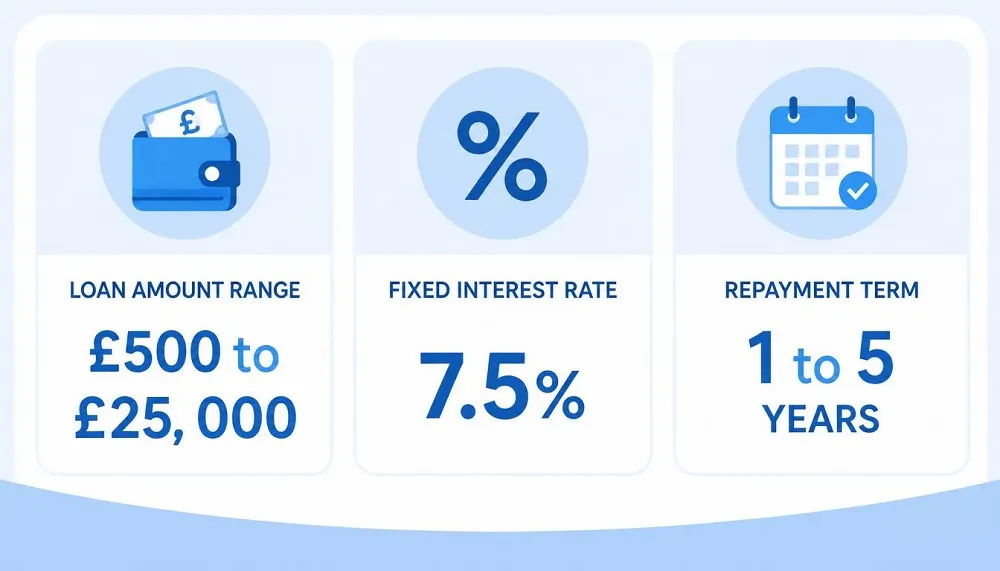

You can borrow between £500 and £25,000. It’s unsecured, so you don’t need to put up your house, savings or any other asset as security. Every successful applicant also gets a dedicated business adviser to help with the application, plus the option of 12 months of free mentoring once the loan is approved.

The important detail people often miss: this is a personal loan, not a business loan. It sits on your personal credit file, and you’re personally responsible for repaying it, even though the money goes into your business.

| Feature | Start Up Loan | Business Grant | Bank Loan |

|---|---|---|---|

| Repayment Required | Yes | No | Yes |

| Interest | Fixed | None | Varies |

| Security | Unsecured | Not applicable | May be required |

| Typical Use | Startups | Specific projects | Established businesses |

| Government Backed | Yes | Often | Not usually |

How Do Start Up Loans UK Actually Work?

The process runs in three stages. First, pre-application support helps you shape your business plan and cash flow forecast. Second, you receive the loan itself, either as a single lump sum or in tranches. Third, you get access to mentoring and business support for up to a year afterwards.

Because it’s backed by government funding rather than pure commercial risk appetite, the scheme exists specifically to fund businesses that mainstream banks tend to turn down, usually because they have no trading history, no assets and no collateral to offer.

Each partner or director in a business can apply individually for up to £25,000, with a cap of £100,000 per business overall. So a two-person partnership could potentially access £50,000 combined, each under their own personal loan agreement.

Start Up Loans UK Interest Rate in 2026: What Changed

This is where a lot of older content gets it wrong. From 2012 until April 2026, the fixed rate was 6% per year. From 6 April 2026, the rate rose to a fixed 7.5% per year for all new applications. If you took out a loan before that date, your original 6% rate still applies for the life of that loan.

There are no application fees and no early repayment charges. You repay over a term of one to five years, and the rate stays fixed for the whole term, so your monthly payment won’t move even if wider interest rates rise or fall.

Eligibility also changed alongside the rate. Previously you could only apply for a first Start Up Loan if your business had been trading for up to 36 months. That’s now been extended to 60 months, meaning slightly more established early-stage businesses can qualify.

Who Is Eligible for a Start Up Loan?

The core eligibility rules are straightforward:

- You must be 18 or over

- You must live in the UK and have the right to work here

- Your business must be based in the UK

- Your business must be trading for no more than 60 months, or not yet trading at all

- You need a workable business plan and cash flow forecast

There’s no minimum credit score published, but the Start Up Loans Company does run a personal credit check as part of the assessment. Certain business types are excluded, including some finance and property investment activities where the borrower would mainly earn commission rather than run a genuine trading business. It’s worth checking the full list of exclusions on the official Start Up Loans site before you spend time on an application.

Start Up Loans UK “No Credit Check”: Setting Expectations

A lot of people search for start up loans UK no credit check, hoping to skip the credit assessment stage entirely. It’s worth being straightforward about this: no legitimate UK lender, government-backed or otherwise, offers meaningful business or personal finance with zero credit check. Any site claiming otherwise is either misleading you or offering something far more expensive and risky, such as unregulated short-term credit.

What genuinely helps if your credit history is thin or bumpy is preparation rather than avoidance. A clear business plan, a realistic personal survival budget, and evidence you can manage the loan repayments will carry more weight with the assessor than a perfect credit score alone. The dedicated business adviser assigned to you during the application can also help present your case in the strongest possible light.

Start Up Loans UK for Bad Credit

If your credit file has missed payments, defaults or a low score, you’re not automatically ruled out. The scheme was built partly to help people who mainstream banks reject, and a poor credit history is one of the most common reasons for that rejection.

That said, the assessment does look at affordability. If your current personal finances suggest you’d struggle to make the repayments on top of your existing commitments, that’s likely to count against you more than the credit score itself. Bringing down other short-term debt before you apply, and being upfront about past credit issues in your application, both tend to help.

Start Up Loans UK vs Business Start Up Grants

These two options get confused constantly, so here’s the practical difference. A business grant doesn’t need to be repaid, but it’s usually restricted to a specific sector, region or purpose, competition for it is fierce, and the application process can take months with no guarantee of success.

A Start Up Loan does need to be repaid, with interest, but it’s far more predictable. If you meet the eligibility criteria and your business plan stacks up, your chances of approval are considerably higher than winning a grant, and the money typically arrives faster.

Most founders are better served treating these as complementary rather than either/or. Use a loan for guaranteed, timely funding, and apply for relevant grants alongside it if your sector has any available.

Start Up Loans UK: Direct Lender or Not?

Searches for start up loans UK direct lender usually come from people wanting to avoid brokers or comparison middlemen. Technically, the Start Up Loans Company itself is the lender behind the government scheme, though the government-backed route works through a network of delivery partners around the country who help process applications regionally.

If you’d rather deal with a single high-street name instead, several banks and specialist providers offer their own unsecured start up business loans outside the government scheme. These tend to have higher rates and stricter trading history requirements, but the application can sometimes move faster since there’s no mentoring component to build in.

How to Apply for a Start Up Loan UK: Step by Step

- Check eligibility online. A short form confirms whether you meet the basic criteria before you invest time in a full application.

- Register and get matched with a business adviser. This person reviews your plan and supports you through the paperwork.

- Submit your business plan, cash flow forecast and personal survival budget. These three documents form the backbone of the assessment.

- Pass the personal credit check. This happens once your supporting documents are ready to submit.

- Receive your decision. Well-prepared applications can be approved within about a month, though it can take longer if documents need reworking.

- Get your funds and start your mentoring. Successful applicants can access up to 12 months of free one-to-one support.

Applications generally need to be completed within 90 days of your initial eligibility check, so don’t start the process until you’re genuinely ready to see it through.

Documents You’ll Need Before You Apply

Having these ready in advance speeds things up considerably:

- A written business plan covering your product or service, market and competitors

- A cash flow forecast for at least the first 12 months

- A personal survival budget showing your household costs alongside the loan repayments

- Proof of identity and UK residency

- Basic financial information if your business is already trading

If you haven’t put a business plan together yet, our step-by-step guide to writing a business plan walks through exactly what to include for a lender-ready document.

What Can You Use a Start-Up Loan For?

The loan is flexible and can cover most genuine start-up and growth costs, including equipment, stock, rented premises, marketing, website development, and working capital while you build up trading income. It’s worth mapping this against your actual start-up costs before you decide how much to borrow, so you’re not over- or under-estimating what you need.

What it can’t be used for includes repaying existing debt, funding training or education courses, or backing investment opportunities that aren’t part of a genuine ongoing business.

| Allowed Uses | Not Allowed |

|---|---|

| Equipment | Personal expenses |

| Stock | Existing personal debt |

| Marketing | Investment activities outside the business |

| Website development | Education or training courses (where excluded by the scheme) |

| Working capital |

Start Up Loans UK Login: Managing Your Account

Once you’ve applied or been approved, you’ll manage your application and repayments through the official Start Up Loans or British Business Bank portal rather than through a generic banking app. If you’re searching for “British Business Bank start up loans login” because you can’t find your sign-in page, go directly to the official startuploans.co.uk site rather than a search result, since there are unofficial pages that mimic government finance schemes to harvest personal details.

Pros and Cons of Government-Backed Start Up Loans

Advantages:

- No security or collateral required

- Fixed rate for the whole term, so repayments are predictable

- No application fee and no early repayment charge

- Free mentoring included for a year

- Genuinely accessible to businesses mainstream banks turn down

Drawbacks:

- It’s a personal loan, so you’re liable even if the business fails

- The maximum of £25,000 per person may not be enough for capital-intensive businesses

- A credit check is required, and missed repayments affect your personal credit file

- The application takes real preparation, not just a quick form

Alternatives to Start Up Loans UK

If a Start Up Loan doesn’t fit, a few other routes are worth comparing. Business start-up grants suit specific sectors or regions and don’t require repayment. Peer-to-peer or challenger bank business loans can offer faster decisions, though often at a higher rate. Asset finance can work well if most of your funding need is equipment rather than cash flow. And for very early, pre-revenue ideas, some founders combine a smaller Start Up Loan with angel investment or crowdfunding rather than relying on one source alone.

Best Start Up Loans UK: How to Compare Sensibly

“Best” depends entirely on your situation rather than a single universal answer. If you have no trading history and limited assets, the government-backed scheme is usually the strongest starting point simply because of its accessibility and fixed, unsecured terms. If you’re already trading with a couple of years behind you and stronger cash flow, a commercial lender might offer a larger amount, even if the rate is higher.

Before comparing, it helps to have your business bank account already set up, since most lenders will ask for one as part of the application, and a dedicated business account also makes your cash flow forecast far easier to build accurately.

Common Mistakes to Avoid When Applying

The most frequent reason for rejection isn’t a poor credit score; it’s an unrealistic cash flow forecast or a business plan that doesn’t clearly explain how the loan will be repaid. Other common mistakes include applying before your documents are ready, underestimating personal living costs in the survival budget, and not accounting for tax or National Insurance when projecting income. Taking the time to get these details right before you submit makes a genuine difference to your chances of approval.

Frequently Asked Questions

Is a Start Up Loan the same as a government grant?

No. A Start Up Loan must be repaid with interest. A grant doesn’t need to be repaid but is harder to get and usually restricted by sector or region.

How much can I borrow with a Start Up Loan?

Between £500 and £25,000 per person, up to a maximum of £100,000 per business across all partners.

What’s the current interest rate?

A fixed 7.5% per year for applications made from 6 April 2026 onwards. Loans taken out before that date keep their original 6% rate.

Will applying affect my credit score?

Yes, a personal credit check is carried out, and missed repayments can affect your credit file, since this is a personal loan.

How long does approval take?

A well-prepared application can be approved within about a month, though it varies depending on how quickly documents are ready.

Final Thoughts

A Start Up Loan can be one of the most accessible ways to fund a new UK business, particularly if you have no assets to offer as security and no trading history yet. The rate has gone up this year, and it’s worth building that 7.5% figure into your cash flow forecast rather than the outdated 6% still floating around online. Get your business plan and survival budget genuinely solid before you apply, and you’ll give yourself the best possible chance of approval.

Author: Daniel Hughes is a UK-based business finance writer with seven years of experience covering SME funding, government-backed lending schemes and small business start-up costs for British finance publications.