Every year, hundreds of thousands of people in the UK turn an idea into a registered business. In the 2024 financial year alone, Companies House recorded 890,684 new company incorporations, an 11.2% jump from the year before. That kind of growth tells you two things: starting a business here is genuinely accessible, and you are not the only one figuring it out right now.

This guide walks through the entire process in the order you will actually need it: validating your idea, choosing a structure, registering with the right government bodies, understanding tax, opening a bank account, sorting licences and insurance, funding your launch, and staying compliant once you are trading. Whether you are a UK resident leaving employment for the first time or an overseas entrepreneur exploring the UK market, you will find the practical details missing from most generic checklists, including the real costs in 2026.

Quick Takeaways

- You can register as a sole trader for free with HMRC or set up a limited company through Companies House for £100 online (or £124 by post) as of 2026.

- Sole traders pay Income Tax through Self Assessment; limited companies pay Corporation Tax at 19% on profits up to £50,000 and 25% above £250,000, with marginal relief in between.

- You must register for VAT once your taxable turnover passes £90,000 in 12 months, though you can register voluntarily earlier.

- Non-UK residents can own and direct a UK limited company without needing to live in the UK, though operating from within the UK usually requires a visa.

- Government-backed Start Up Loans range from £500 to £25,000 and come with free mentoring.

- Around 1 in 5 new UK businesses do not make it past their first year, and roughly 39% survive to five years, so planning for cash flow matters as much as the paperwork.

Is the UK a Good Place to Start a Business?

The UK remains one of the more straightforward places in the world to register and run a small business. You can form a limited company online in around 24 hours; there is no minimum share capital requirement for most companies, and a sole trader can begin trading immediately and register with HMRC later, as long as it happens within the same tax year that profits exceed £1,000.

The wider environment helps too. London consistently ranks among the strongest global startup hubs for access to talent and research, and government schemes like Start Up Loans and regional Growth Hubs exist specifically to support people taking their first steps into business ownership. None of that guarantees success, but it does mean the administrative side of starting up rarely needs to be the bottleneck.

Step 1: Validate Your Business Idea

Before any registration happens, spend real time testing whether people will actually pay for what you are offering. This is the step most first-time founders rush, and it is also the step that determines whether everything that follows is worth doing.

Practical validation does not require a big budget. Talk to potential customers directly, run a small pre-sale or waitlist, or offer a limited version of your service to a handful of people at a fair price. Pay close attention to objections, not just compliments. If three different people hesitate on price, that is more useful information than ten people saying “I’d definitely buy that” without reaching for their wallet.

Once you have early signal, sketch a simple one-page business plan covering what you sell, who buys it, how you will reach them, what it costs to deliver, and how much you need to get to your first ten paying customers. You do not need a 40-page document to register a business, but you do need enough clarity to avoid registering a structure that does not fit how you actually plan to operate.

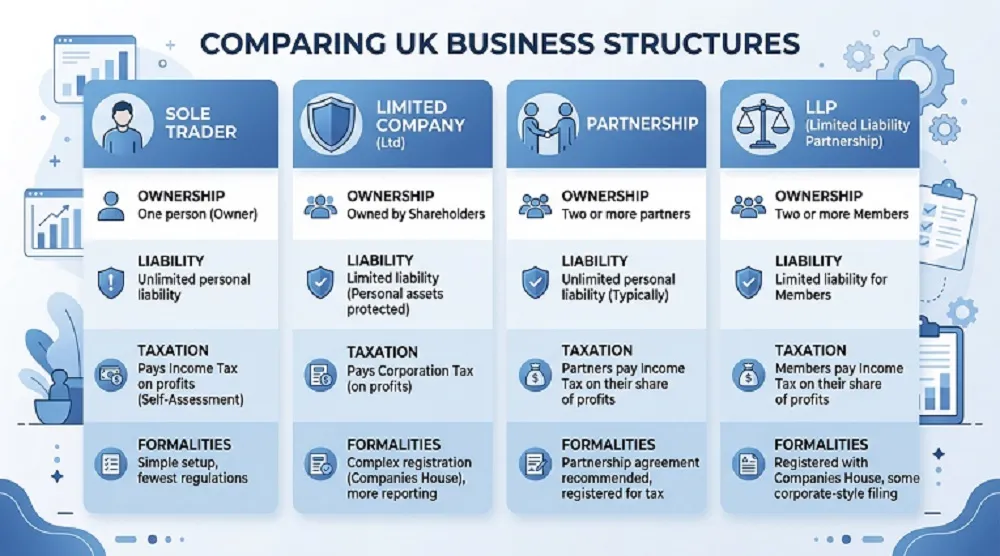

Step 2: Choose the Right Business Structure

Your structure affects how you pay tax, how much paperwork you handle, and how exposed your personal assets are if something goes wrong. Most new businesses choose between four options.

Sole Trader

You and the business are legally the same entity. It is the simplest structure: minimal paperwork, no Companies House registration, and you keep all profits after tax. The trade-off is unlimited liability, meaning your personal assets are not legally separated from business debts. This suits freelancers, consultants, tradespeople, and anyone testing an idea with low risk and modest turnover.

Limited Company

A limited company is a separate legal entity from its owners. Your personal liability is limited to what you have invested in shares, which protects your personal assets if the business runs into debt. It involves more admin (annual accounts, a confirmation statement, and Corporation Tax filings), but it is also more tax-efficient once profits grow, and it tends to look more credible to clients, suppliers, and investors.

Business Partnership

Two or more people share responsibility for the business and its debts, similar to a sole trader structure but split across partners. Profits are divided, and each partner pays Income Tax individually through self-assessment on their share.

Limited Liability Partnership (LLP)

An LLP combines partnership flexibility with limited liability protection, similar to a limited company. It is popular with professional services firms (solicitors, accountants, architects) where multiple partners want to share ownership without exposing personal assets to the full extent of business debt.

Which Structure Should You Choose?

| Factor | Sole Trader | Limited Company |

|---|---|---|

| Liability | Unlimited, personal assets at risk | Limited to your shareholding |

| Setup cost | Free | £100 online (2026) |

| Ongoing admin | Low (Self Assessment) | Higher (annual accounts, confirmation statement) |

| Tax | Income Tax via Self Assessment | Corporation Tax, plus tax on how you withdraw money |

| Public record | None | Director and company details are public |

| Best for | Testing ideas, low-risk freelance work | Growing businesses, higher profits, outside investment |

There is no universally “better” option. A general rule many accountants use: if your annual profit is comfortably under £30,000 to £40,000 and risk is low, sole trader status is often simpler and just as tax-efficient. Above that range, or in higher-risk trades, a limited company frequently starts to make more financial and legal sense. It is also worth knowing that moving from sole trader to limited company later is a well-trodden, straightforward path, so starting simple is rarely a wrong move.

Step 3: Register Your Business

Registering as a Sole Trader

You can start trading as a sole trader immediately. The only legal requirement is registering for Self Assessment with HMRC, and you must do this if you earn more than £1,000 in a tax year (6 April to 5 April). Registration is free and done online through your Government Gateway account. Missing the deadline (three months after starting self-employment, in practice) can trigger a financial penalty, so it is worth registering as soon as trading begins rather than waiting.

Registering a Limited Company

Limited company registration happens through Companies House, either directly online or via an authorised formation agent. You will need:

- A company name that is not identical or too similar to an existing one (check using the Companies House name search)

- A registered office address in the UK

- At least one director aged 16 or over

- At least one shareholder

- Details of People with Significant Control (PSC)

- A simple statement of how the company will be run (most new companies use standard model articles)

Online registration is typically processed within 24 hours. Once incorporated, you also need to register separately for Corporation Tax with HMRC within three months of starting to trade.

How Much Does It Cost in 2026?

| Item | Cost |

|---|---|

| Sole trader registration with HMRC | Free |

| Limited company incorporation (online) | £100 |

| Limited company incorporation (paper) | £124 |

| Annual confirmation statement (online) | £50 |

| Annual confirmation statement (paper) | £110 |

These figures reflect the Companies House fee increase that took effect on 1 February 2026, part of wider reforms under the Economic Crime and Corporate Transparency Act aimed at improving the accuracy and security of the UK company register. Budget for these as ongoing costs, not just one-off setup fees, since the confirmation statement is filed every year.

Step 4: Understand Your Tax Obligations

Tax confusion is one of the most common reasons new business owners feel overwhelmed, but the structure of UK business tax is more logical than it first appears.

Income Tax and Self Assessment

Sole traders and partners pay Income Tax on business profits through an annual Self Assessment return, using the same personal tax bands that apply to employment income. Good record keeping from day one (income, expenses, receipts) makes this far less stressful when the filing deadline approaches.

Corporation Tax

Limited companies pay Corporation Tax on profits, not on turnover. For the 2025/26 tax year, the rate is 19% (the small profits rate) for profits up to £50,000, and 25% (the main rate) for profits over £250,000. Profits between those two thresholds qualify for marginal relief, which gradually scales the effective rate between 19% and 25% rather than jumping straight to the top rate. This detail matters because many founders assume hitting £50,001 in profit suddenly costs them the full 25% rate, which is not how the system works.

VAT

You must register for VAT once your taxable turnover exceeds £90,000 in any rolling 12-month period. You can also register voluntarily below that threshold, which some businesses do to reclaim VAT on expenses or to appear more established to larger commercial clients.

National Insurance and PAYE

Sole traders pay National Insurance contributions based on profit levels, which also count toward State Pension eligibility. If you take on employees, whether you are a sole trader or a limited company, you must register as an employer with HMRC and operate PAYE to handle their tax and National Insurance correctly, even if you are the only person on the payroll.

Step 5: Open a Business Bank Account

A separate business bank account is not strictly required by law for sole traders, but it is required for limited companies, since company money is legally separate from personal money. Even for sole traders, separating finances early avoids a tangled mess of personal and business transactions that makes bookkeeping, tax returns, and even mortgage or loan applications far harder later. Most UK banks offer dedicated business accounts with free periods for new businesses, and several digital-only providers now offer same-day account opening.

Step 6: Sort Out Licences, Permits, and Insurance

Not every business needs a licence, but many do, depending on the activity. Food businesses, businesses selling alcohol, taxi services, and certain home-based businesses (depending on local council rules) typically need specific permits. GOV.UK’s licence finder tool is the quickest way to check what applies to your specific trade and location.

Insurance is a separate but related consideration. If you employ staff, employer’s liability insurance is a legal requirement, even if you only employ one person part-time. Many service-based businesses also carry professional indemnity insurance to cover claims of negligent advice or work, and public liability insurance if customers visit your premises.

Step 7: Fund Your Business

Most small businesses start with a mix of personal savings and careful budgeting, but several funding routes exist if you need more than you have on hand.

- Personal savings: The most common source, with no interest or equity given away, but it puts personal financial security at risk if the business does not perform as expected.

- Start Up Loans: A government-backed scheme offering loans from £500 to £25,000 at a fixed rate, paired with free mentoring for the first year.

- Small business grants: Non-repayable funding, often sector or region-specific, available through local councils or bodies like Innovate UK, though competition is typically high.

- Crowdfunding: Raising smaller amounts from a large number of backers, often in exchange for early product access or rewards rather than equity.

- Angel investors or venture capital: Suited to high-growth businesses with scalable models, usually in exchange for equity, and considerably more competitive to secure.

A practical first step regardless of funding route: calculate your actual startup costs and the working capital you need to survive the first three to six months before revenue stabilises. Most lenders and investors will expect to see this in some form before committing money.

Starting a Business in the UK as a Non-UK Resident

Foreign nationals can own and direct a UK private limited company without needing UK citizenship or residency. There are no restrictions on foreign ownership when registering with Companies House, and you do not need to live in the UK to be listed as a director or shareholder.

Where it gets more involved is if you intend to physically operate the business from inside the UK, for example running a shop, working day-to-day from a UK office, or actively managing operations on the ground. In that case, you typically need an appropriate visa, such as the Innovator Founder Visa for genuinely new and innovative business ideas. Decisions on applications made from outside the UK are usually returned within about three weeks, compared with around eight weeks for applications made from inside the country. It is worth noting that older routes like the Tier 1 Entrepreneur Visa and the original Start-up Visa are no longer available, so always check current GOV.UK guidance rather than older articles when planning this step.

Many non-resident founders also choose to appoint a local director or use a registered Authorised Corporate Service Provider, since this can simplify identity verification requirements and make opening a UK business bank account considerably easier.

Your First Year Compliance Calendar

Registration is the beginning, not the finish line. Here is a simplified view of what typically follows in year one:

| When | What’s due |

|---|---|

| Within 3 months of starting to trade | Register for Corporation Tax (limited companies) |

| By 5 October following the tax year | Register for Self Assessment if newly self-employed and not yet registered |

| Ongoing | Keep accurate records of income, expenses, and receipts |

| Once turnover passes £90,000 (rolling 12 months) | Register for VAT |

| Annually | File a confirmation statement with Companies House (limited companies) |

| Annually | File accounts with Companies House (limited companies) |

| Annually | Submit a self-assessment return (sole traders, partners, and most directors) |

Setting calendar reminders for these dates, or using accounting software that tracks them automatically, removes a significant amount of stress later. Late filings with both HMRC and Companies House carry financial penalties that are entirely avoidable with basic planning.

Why UK Businesses Fail (and How to Avoid It)

It is worth being honest about the numbers rather than only focusing on the exciting part of starting up. According to Office for National Statistics data, the five-year survival rate for UK businesses born in 2018 was 39.4%, and various industry estimates suggest roughly one in five new businesses do not make it through their first year. These figures are not meant to discourage anyone; they are meant to set realistic expectations.

The businesses that beat these averages tend to share a few habits: they keep a close eye on cash flow rather than just profit on paper, they separate personal and business finances from day one, they stay on top of tax deadlines instead of scrambling at the last minute, and they continue validating demand even after launch rather than assuming early success will simply continue. Treating the administrative side of the business (registration, tax, record keeping) as seriously as the product or service itself is one of the most underrated predictors of staying power.

Frequently Asked Questions

Do I need to register a business name in the UK? Sole traders can trade under their own name or a chosen trading name without a formal registration process, though the name cannot be identical to an existing registered trademark or imply a connection to government. Limited companies must register a unique company name with Companies House as part of incorporation.

Can I run a UK business from home? Yes, and many new businesses start this way to reduce costs. You may still need to check your mortgage or lease terms, inform your home insurer of business use, and confirm whether your local council requires any specific permissions depending on the type of activity.

How long does it take to register a limited company? Online registration through Companies House is typically processed within 24 hours, though it can take longer during busy periods or if additional identity checks are required.

What is the difference between a trading name and a registered company name? A registered company name is the legal name recorded at Companies House and used on official documents. A trading name (sometimes called a “doing business as” name) is the name customers see day to day and can differ from the registered name, as long as it follows naming rules and is not misleading.

Do sole traders need to file accounts with Companies House? No. Filing accounts and a confirmation statement with Companies House only applies to limited companies and LLPs. Sole traders report their income and expenses through an annual Self Assessment return to HMRC instead.

Conclusion

Starting a business in the UK is genuinely achievable without a legal team or a large budget, but it works best when the steps happen in the right order. Validate the idea first, choose the structure that matches your risk tolerance and growth plans, register with the correct body for that structure, and then build tax, banking, and compliance habits before they become urgent rather than after. The current costs are modest (free for sole traders, around £100 for an online limited company registration in 2026), and the support available through Start Up Loans, Growth Hubs, and the British Library’s Business and IP Centre network means you are rarely figuring this out entirely alone.

The honest survival statistics are worth holding onto, not as a warning to stay employed, but as a reason to take the unglamorous parts seriously: record keeping, cash flow, and deadlines. Founders who treat those basics as part of the business, not a distraction from it, give themselves a real edge over the average.

If you are ready to move from research to action, the next concrete step is simple: decide which structure fits your situation today, then register through GOV.UK or Companies House directly. You can always change the structure as the business grows, but you cannot get back the months spent waiting for “the perfect moment” to begin.